Unveiling the Future: AssetMetrix’s Cutting-Edge Forecast Model

- Christian Tausch

- 19.10.2023

- 4 min read

- Christian Tausch

- 19.10.2023

- 4 min read

In the ever-evolving landscape of private equity, precision and foresight are the keys to success. Throughout 2023, AssetMetrix embarked on a journey to redefine the industry’s future with a groundbreaking Forecast Model. This blog post takes you into the world of private equity forecasting, powered by AssetMetrix’s innovative approach.

Predicting Tomorrow with Confidence

AssetMetrix’s Forecast Model is a powerful tool designed to predict future cash flows and net asset values (NAVs) of private capital funds and portfolios. It stands on the bedrock of analytical soundness and well-founded statistical principles. At its core, the model embraces the reduced form approach to cash flow modeling, a technique that offers an elegant and efficient solution.

Building on a Solid Foundation

AssetMetrix’s model isn’t born out of thin air—it’s an enhanced version of Buchner et al.’s work from 2010, with insights drawn from Tausch et al.’s [2022] deal-level equivalent. This lineage ensures that the model is firmly rooted in proven methodology. The forecasting engine itself is a comprehensive suite of econometric models, fueled by the current macroeconomic environment and informed by established results from public market literature.

Mastering the Art of Incomplete Information

Private equity comes with its unique set of challenges, notably data scarcity and the approximative nature of fund NAVs. AssetMetrix’s modelling approach thrives on overcoming these hurdles. The model is intentionally designed for settings with incomplete information, following the wisdom of Jarrow and Protter [2012]. This resilience is what sets the AssetMetrix model apart.

The Power of Probabilistic Modeling

Private capital funds are inherently cash-flow-driven, and AssetMetrix recognizes this fact. That’s why our forecasting engine primarily focuses on the probabilistic modeling of fund cash flows. This approach inherently allows the derivation of probability bands around expected values, a vital component for managing downside risk effectively.

A Glimpse into the Future: 2023 and Beyond

In 2023, AssetMetrix took a significant step forward by re-estimating and updating the forecast model parameters. The process involved employing standard statistical and econometric estimation procedures, fine-tuning model parameters through hyperparameter tuning, and utilizing a simulation tool to validate and backtest the model. This commitment to precision and validation ensures that the forecast model remains on the cutting edge.

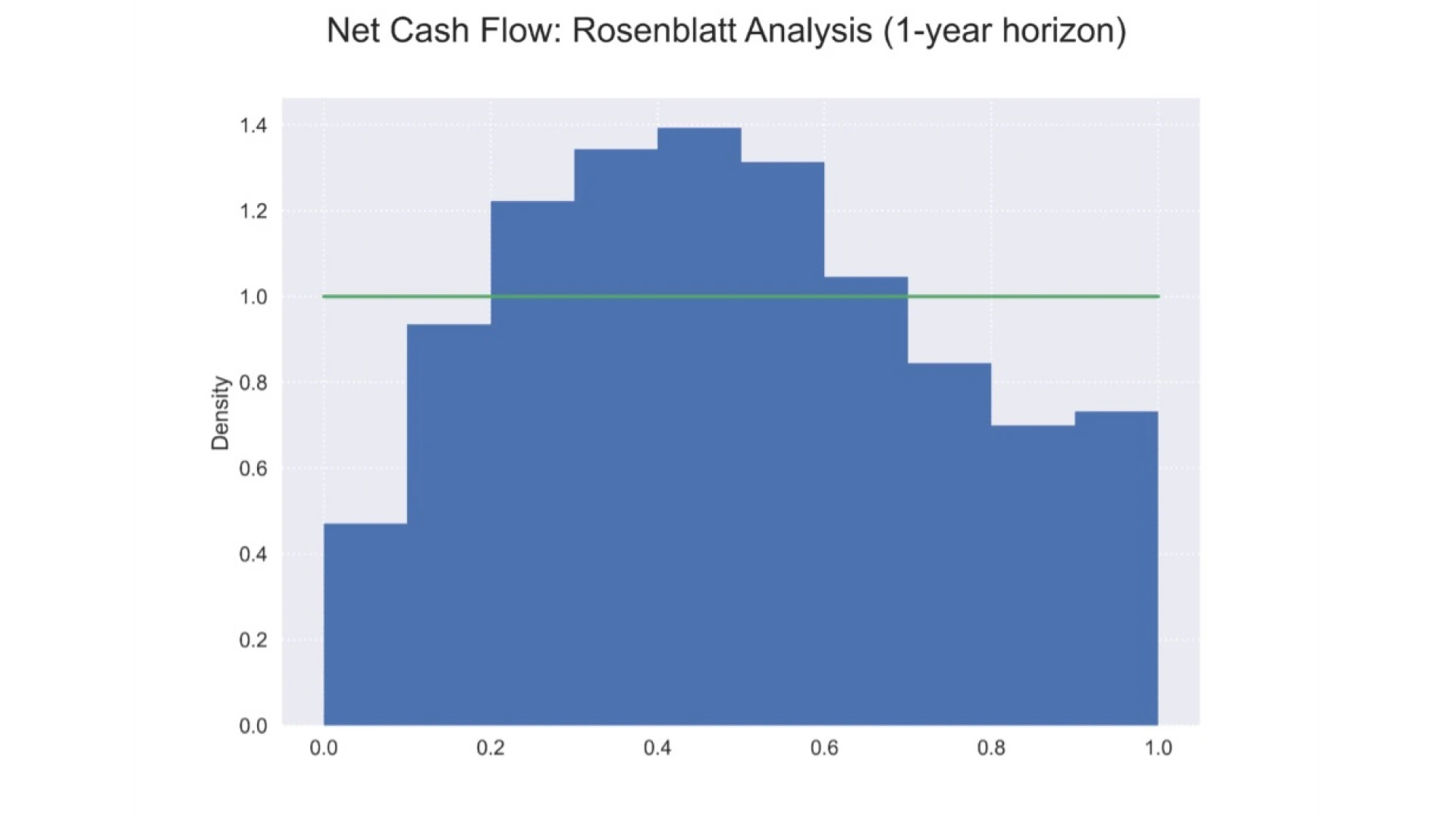

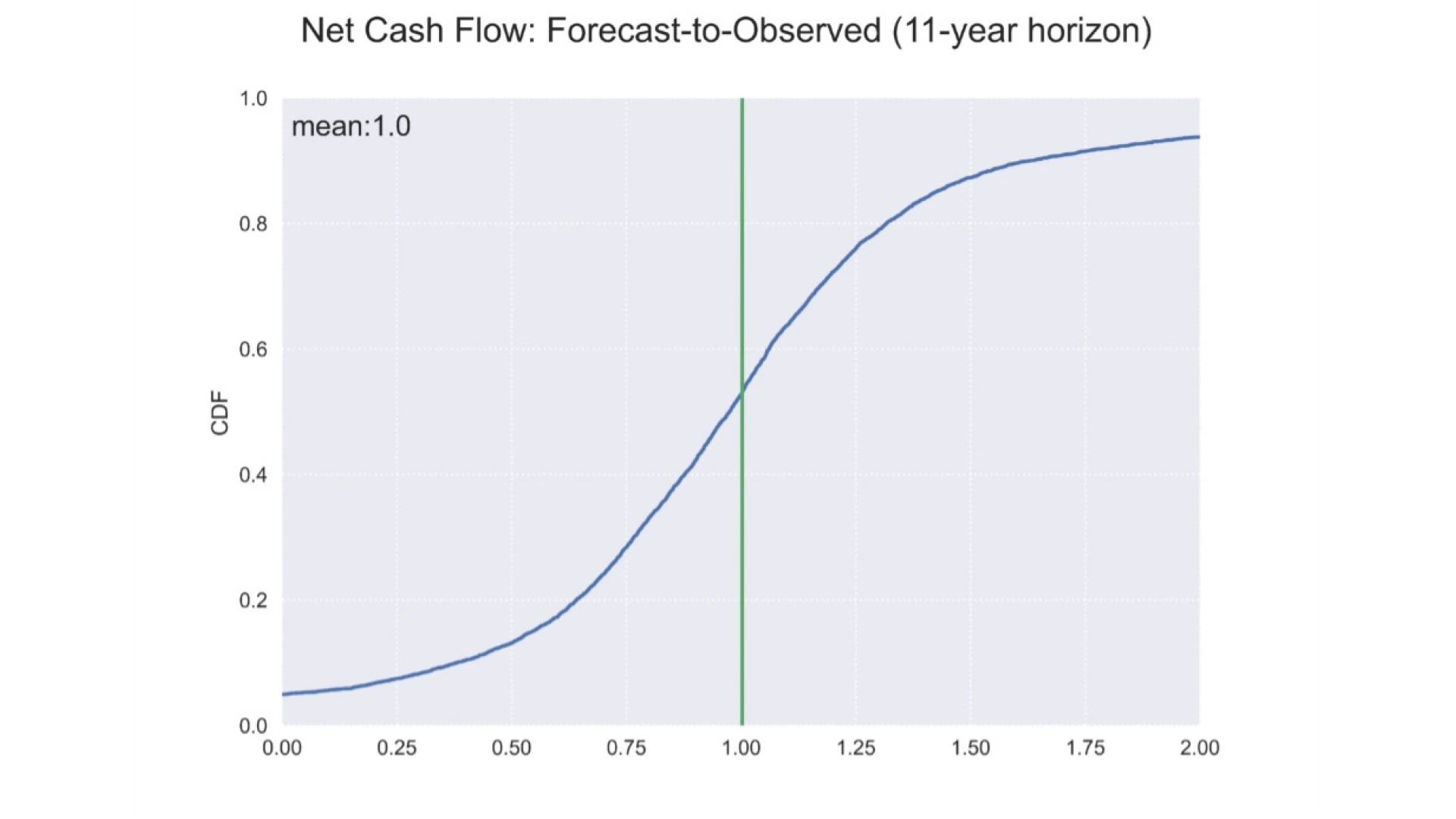

Net Cash Flow Backtest Results

In the world of private equity, net cash flow (NCF) stands as a paramount KPI. It’s not just about short-term liquidity planning and treasury management; it also informs investors about break-even timing and final fund performance. AssetMetrix understands the significance of NCF and has rigorously tested its forecast model in terms of NCF (besides all other important KPIs). Generally, the precision of AssetMetrix’s forecast has seen consistent improvements at each step of the estimation and fine-tuning procedure. These improvements hold true for various forecast horizons (1, 3, 5, 7, and 11 years) and for both the (in-sample) estimation and (out-of-sample) validation sets.

In the next three figures, we exemplarily summarize the NCF results over varying forecast horizons in the validation set.

Figure 1 depicts a so-called Rosenblatt transformation analysis where we input the empirically realized values in the model-implied probability distribution to backtest our forecast probability bands. The transformed distribution should then come close to a uniform distribution if our model describes the empirical distribution of the NCF adequately [Rosenblatt, 1952]. Figure 1 illustrates that our model generally has probability bands that fit nicely (close to uniform) but are still conservatively calibrated (fewer tail observations); this holds for all KPIs and forecast horizons.

Figure 2: High medium-term precision

Figure 2 shows that a very high R^2 of 95% can be achieved for the medium five-year horizon; even for the 11-year horizon, we obtain an impressive 88% R^2.

Figure 3: High long-term precision.

Figure 3 demonstrates that even for a 11-year horizon, the forecast model can produce unbiased NCF estimates as the forecast-to-observed ratio of the Net Cash Flow is on average exactly one.

In essence, AssetMetrix’s commitment to precision is paying off, and these backtest results reinforce the model’s capability to deliver accurate Net Cash Flow forecasts for short-, medium- and long horizons – a critical component in the world of private equity.

Validation That Matters

Our full forecast backtest report dives into the nitty-gritty of the model’s validation process. It explores the data used for estimation and backtesting, providing a comprehensive summary of validation results for all forecast components:

Contributions

Distributions

Net Cash Flow

Net Asset Value

TVPI Ratio

These components are at the core of private equity forecasting, and AssetMetrix’s model delivers very accurate results in this dynamic world.

In conclusion, AssetMetrix’s Forecast Model is revolutionizing cash flow and performance forecasting in the private equity industry. It’s a tool that combines statistical prowess with innovative thinking, offering a glimpse into the future with confidence. In a world where precision is paramount, AssetMetrix is setting the gold standard for private equity forecasting. The future looks brighter than ever.

Sources

Buchner, Kaserer, Wagner – Modeling the cash flow dynamics of private equity funds: Theory and empirical evidence (2010)

Jarrow, Protter – Structural versus Reduced‐Form Models: A New Information‐Based Perspective (2012)

Rosenblatt – Remarks on a Multivariate Transformation (1952)

Tausch, Buchner, Schlüchtermann – Modeling the exit cashflows of private equity fund investments (2022)