**Portfolio Analytics** comprises all quantitative models and evaluations that provide investors, fund managers, and other market participants with in-depth analyses of private equity portfolios. The spectrum of possible applications ranges from benchmarking, risk analyses, and stress tests to cash flow and performance forecasts. In addition, tools for planning future private capital investments and for modelling fund-internal cost structures are offered.

Note: In the following, the term "private equity" is replaced by the broader term "private capital", which also includes segments such as private debt, real estate and infrastructure.

In this article the following aspects will be discussed in more detail:

The performance of private capital investments has traditionally been measured using metrics such as Total Value-to-Paid-In (TVPI) or Internal Rate of Return (IRR). However, these condensed individual values on their own have only limited informative value – they should therefore be compared with similar investments in the private or public capital market within the framework of benchmarking. Only such a comparison provides meaningful information about the success or failure of the investment strategy of the portfolio under consideration.

However, decisions on the composition of the portfolio also influence the risk to which the invested capital is exposed. To make this transparent, key figures such as value-at-risk and correlations between portfolio components and stock or sector-specific indices can be used. By including macroeconomic scenarios, stress testing relating to future performance is also possible.

A look into the future is provided by cash flow forecasting based on the specific composition and history of the private capital portfolio under consideration. The modelling of cash inflows and outflows and the performance of various types of funds is based on the analysis of empirically observed data from the private capital market and also takes the macroeconomic environment into account.

Further support can be provided by analysis tools that help to plan the amount and type of new investments required for an existing or to be built up private capital portfolio over the coming years. This is usually done in order to achieve predetermined strategy or allocation targets within the framework of overall portfolio planning.

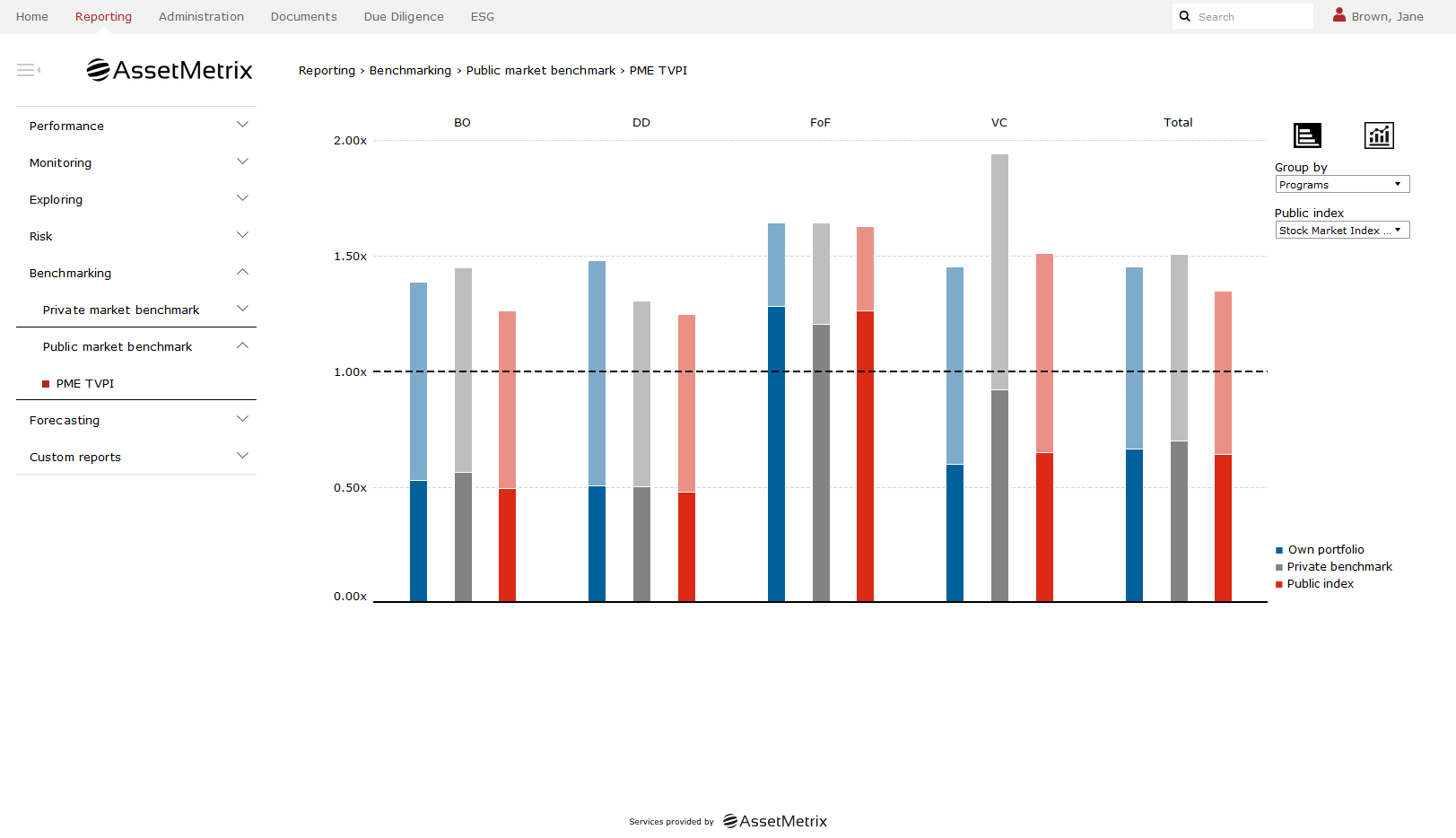

There are basically two ways to compare the performance of private capital portfolios: Either similar investment opportunities (funds of funds, funds, or portfolio companies) within the private capital market are used – in which case we speak of private market benchmarking. On the other hand, one can ask how profitable a similar investment in the public capital market would have been instead – so-called public market benchmarking.

If we look at private capital benchmarking first, it should be noted that a sufficient data basis must be available or established in order to form meaningful peer group buckets for analysis. This is usually done according to the criteria vintage, strategy, and regional investment focus of the fund under consideration. With the help of these peer groups, the performance of each investment object in a portfolio can be classified – for example with a quartile comparison: This allows a statement to be made as to whether the investment under consideration belongs to the top, second, third, or bottom 25 percent of the observed performance distribution compared to similar investments. This methodology can be applied to various indicators, such as Total Value-to-Paid-In (TVPI), Distributed-to-Paid-In (DPI), Residual Value-to-Paid-In (RVPI) or Internal Rate of Return (IRR). Extended approaches such as performance decomposition according to yield drivers or historical simulations for forming quartile comparisons can also be built up on the basis of the peer group analysis.

In the field of public market benchmarking, the task is to make the performance of an alternative investment in the public capital market – usually represented by a suitable stock index – comparable with the cash flows of a private capital portfolio. The methods used for this purpose are summarized under the term Public Market Equivalent (PME). Their basic idea is to transfer contributions and distributions of the private capital portfolio into corresponding simultaneous investments and disinvestments into or out of the public capital market. The invested capital increases in each case based on the performance of the selected benchmark index, so that at any given time the value of this fictitious portfolio can be compared with the value of the private capital portfolio. Depending on the PME method used, the results can be presented in the form of performance multiples (TVPI), IRRs, or market multiples (Kaplan-Schoar PME) and percentual outperformance (Direct Alpha).

The risk of private capital portfolios can be assessed using Value-at-Risk (VaR): On the basis of robust correlation models and in conjunction with expected returns and standard deviations for various private capital segments and target regions, the maximum expected loss amounts can be determined at various confidence levels. The information can be based on a one-year or multi-year period and presented as a relative percentage or as an absolute amount relative to the current value of the portfolio plus any future payment obligations. The inclusion of correlations within the portfolios under review (composed of investments with different years of issue, segments, or regional focus) makes diversification effects visible.

In addition, calculated correlations – between different private capital portfolios or in comparison to market indices – can be used to show the diversification potential with regard to an investor’s overall portfolio. In conjunction with the forecasting of future cash flows (Forecasting, see next section), statements can also be made about the change in expected performance in the event of a change in the macroeconomic environment (stress testing).

If one wants to look into the future and estimate what cash flows and performance can be expected from a private capital portfolio, it is necessary to model all investment objects contained in it over their entire life cycle. A look at past patterns of incoming and outgoing payments of typical sub-segments of the overall market allows the derivation of patterns that can be described by a mathematical formula system. In addition, the identified patterns must be supplemented and modified by the prevailing macroeconomic environment, as this is the key factor determining the expected overall performance of the respective investment.

Within the framework of such a forecast, all future incoming and outgoing payments as well as the quarterly valuations (NAVs, net asset values) can be presented for each investment object individually and also on an aggregated portfolio level. It is also possible to derive all common performance indicators (e.g. TVPI, IRR) for any future point in time up to the end of the portfolio lifetime. In addition, besides the “average path”, which indicates the most probable future development, also probability bands for each predicted variable are a result of the analysis. This makes it easy to estimate how reliable the forecast is or within which value ranges the actual cash flows or performance figures can be expected.

In conjunction with assumptions about planned new investments, forecasting can also be used to plan and optimize the further development of a private capital portfolio. Program planning can be used to keep the value of the portfolio constant over time (either as an absolute amount or as a percentage of an investor’s total portfolio) or to bring it closer to a certain target value. Optimization is also possible within the private capital portfolio – for example, to maintain or achieve a desired strategy distribution or regional diversification.

In principle, the availability of data in the field of private capital is still limited – even if increasing standardization and the emergence of market databases in recent years have created the conditions for deeper analysis. However, unlike in liquid market segments, valuations of investment properties are largely carried out only on a quarterly basis, so that the frequency of data is low. The challenge in the design and development of portfolio analytics is therefore by no means to deal with “big data”, but rather to deal with incomplete data.

As a consequence, all models must be based on robust procedures and, in some cases, be supplemented by expert-based parameterizations in order to deliver meaningful and helpful results. The advantage for the user, however, is that the data requirements for his own private capital portfolio to be analysed remain relatively simple. In many cases, this means that the time-consuming entry of complete data histories can be avoided and instead the analysis can be started with cumulative values from a certain date onwards. The respective contributions and distributions, the quarterly valuations, and some general information on the investment object serve as the basic framework for the portfolio analytics presented above. If detailed data is available, the models can flexibly incorporate this data and offer an equally detailed analysis or presentation of results – but the initial hurdle for using informative portfolio analytics is very low!

We would be delighted to present our Portfolio Analytics module in detail and show you how you can benefit from state-of-the-art analytics as well as which statistical models our analyses are based on.

Further Analytics Insights

As evidenced by recent EU regulations, Liquidity Stress Testing (LST) is a vital topic for Alternative Investment Fund Managers (AIFMs). Find out more about LST solutions.

Liquidity planning and management continue to be crucial topics for private capital funds. In this article, we provide insights on how a sophisticated tool can simplify your planning.

Due to the illiquidity of private capital funds, it is of utmost importance for investors, but also for fund managers, to know exactly the cash flow profile of their portfolio or funds. In the following, we describe our innovative cash flow forecasting engine that facilitates this.

This paper discusses why proper risk measurement for private capital funds is notoriously difficult and how to overcome these challenges.